Page updated / checked 5.1.2025.

Logistics costs are a significant part of the company’s business costs. Logistics costs share of turnover varies depending on company’s industry, size and form of production.

In business, intense competition continues to tighten profitability requirements. Profitability is measured by company’s ability to make profit in the long term. Profitability can be analyzed so that company’s profit is proportioned to turnover or achieved results are compared to resources. The vital condition of the company is that working capital (capital invested in company’s running operation) is sufficient.

Calculation of working capital

Working capital = current assets + trade receivables – trade payables – advance payments received

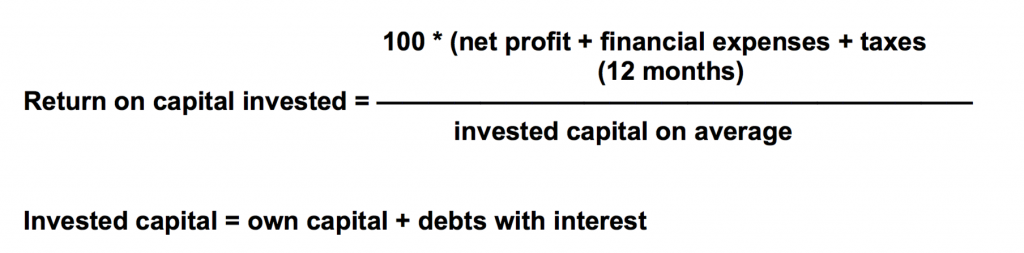

Commonly used indicator of business profitability is return on investment (ROI). It is a key figure, which shows return on capital in percentage.

Calculation of invested capital (%)

ROI indicates the overall profitability rate of invested capital i.e. the capital invested in the business. In company capitals are invested in financial and current assets and working capital. Financial assets (rahoitusomaisuus) are cash and money flows and possibly received from sales advance payments. Current assets (vaihto-omaisuus) include goods for consumption. Fixed assets (käyttöomaisuus) are, for example, production tools and buildings.

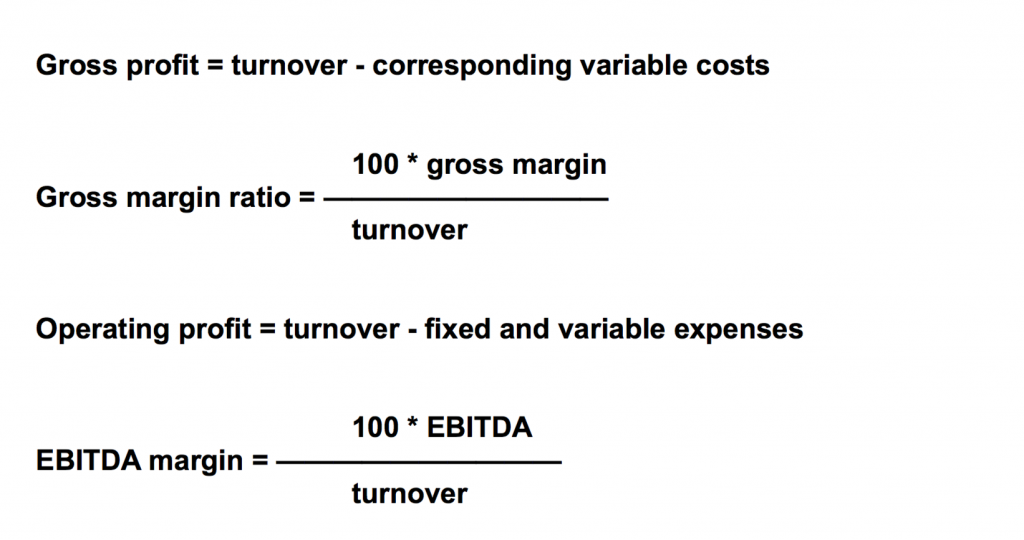

Other indicators

Other profitability business indicators among others are operating margin, gross margin and EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) margin.

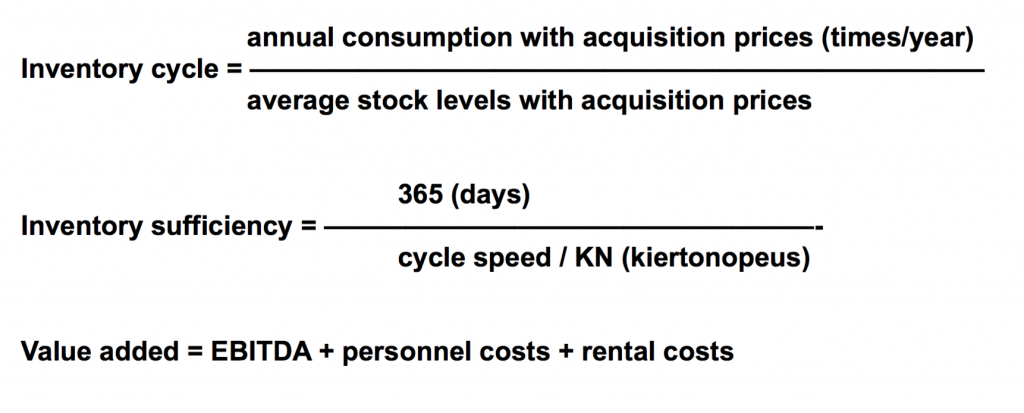

Inventory turnover ratios are inventory cycle (varaston kierto) ja inventory

sufficiency (varaston riitto).

Personnel resources are taken into account in value added (jalostusarvo) and it is an indicator (mittari) of the efficiency of personnel.

Logistics and supply chain performance is measured with indicators and key figures. Just with indicators one can not conclude much before they are being compared to some other number.

Indicators can be financial and non-financial, strategic, tactical and operational as well as external or internal.

All the indicators are not suitable for all companies, but the use of indicators affected by the nature and scope of business.